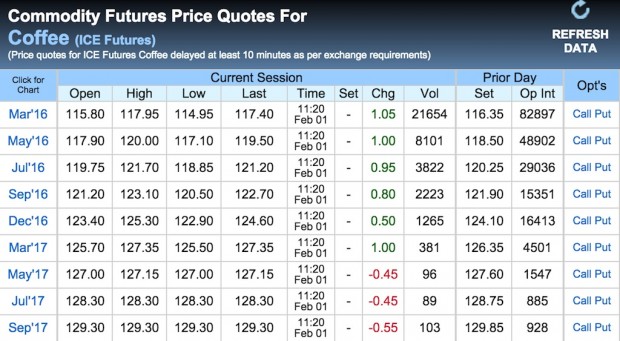

The latest ICE futures prices for coffee as of this publication.

For the final (for now) Price Risk Management conversation, I want to go in a different direction. So far we have heard about a PRM perspective for cooperatives, estates, small farms and from the exporter. Our conversation today is with someone who really understands the mechanics of how price insurance and hedging with futures work.

Albert Scalla is the Executive Vice President at Intl FC Stone, a financial services trading company that is a leader in providing products and services for corporations and cooperatives to deal with price risk. They provide the products and have a first class set of trainings on this topic for importers, exporters, roasters and cooperatives.

The interview was condensed and edited for clarity and took place on January 19, 2016:

KK: Hi Albert. Thanks so much for making the time today. I’d like to start by asking you a broad market analysis question that I get from farmers.How can the market price coffee at these levels? We are at or near the cost of production.

AS: I’d say we’re below cost of production in many countries. So, pricing depends on supply and demand. And in contrary to many analyses, we have a slight over-supply of coffee globally. How much coffee do we have? This is a difficult question to answer due to very inefficient and deficient logistics. We have a slight surplus of coffee at the moment. If we had a slight deficit like the ICO (International Coffee Organization) thinks, we’d be sitting at $1.70. If we had a lack of production or a declining production, we wouldn’t have stocks staying level at this moment.

Pricing is dependent on supply and demand and unfortunately has nothing to do with the cost of production. Additionally, we have had increasing volatility on the production side. Looking ahead to the 2016 cycle, we have Colombia recovering, Honduras is going to put up big numbers, Brazil is recovering from the frost and the market is currently pricing a sizable surplus.

KK: Can you talk about what you mean on the inefficient logistics? Is this because we have difficulty measuring who much coffee we deliver to the market from what we see out in the field?

AS: Let’s take an example: The government of Brazil tomorrow will put out their numbers for the next harvest. Say the estimate of the crop size to be 42 million (Author’s note: The report has since been issued, on Jan. 20 by Conab, the Agricultural ministry’s crop-forecasting agency, which actually estimated 49 to 51.9 million bags.) Most of the commercial entities said 48 million. Commercial entities will betting on this so they have a different point of view. The difference in the estimates is 6 million bags, or the output of Honduras.

Now you look at Indonesia and Vietnam and what comes from there. What’s the true production worldwide? You see how this can be problematic. Now let’s look at consumption worldwide. How do you measure consumption? By the disappearance method. Brazil produces X, exports Y. Z is left as stocks. What disappears is consumption. For consuming countries it’s easier. You look at imports and left overstocks — easier way of calculation.

KK: That’s mind-blowing that the differences in the estimates can be equal to the total production of Honduras. How can producers be protected in this environment?

AS: We went through this exercise at end of the third quarter of 2013. We told farmers not to sell, and to wait for market to go up. We were telling folks to speculate and we taught producers to do variable sales. We also encouraged them to sell now and buy insurance — in case the market does spike up you will participate in the rally. When you sell, your natural expectation thinks the market will go up after the sale. The insurance ensures that you aren’t left out. The biggest fear of a producer is selling his coffee and then the market goes up tomorrow. So this offers a way to sell and to participate in case you are wrong. In early 2014, we gave out checks up to 80 cents a pound. when the price spiked up to $2 a pound.

KK: So walk us through the mechanisms of how a cooperative buys price risk insurance.

AS: They need to access the market. There are two kinds of accounts (at Intl FC Stone). There is a simple account and a structured products account. If a producer comes to cooperative and they can offer the producer protection directly with Intl FC stone and can get the quote for the insurance. For the structured products account, we can basically do fractional hedging, but it has higher financial requirements to open an account.

KK: What are the requirements that a cooperative needs to meet to open an account with Intl FC Stone?

AS: It’s similar to opening an account with a bank. You need to sign some papers, submit a financial statement and fill out some paperwork. For the more advanced account, it has minimum financial requirements set by the government.

KK: What about credit? Do you offer credit to your clients?

AS: We can’t offer credit to purchase options. Options need to be bought with cash to pay the counterparty. There are no lines of credit on insurance premiums.

KK: Can we talk about how options are priced? Are there general rules for how this is priced? I’m assuming that the longer the time frame, the more expensive, and the closer the strike price is to the NYC price, the more expensive the insurance?

AS: Yes, that’s right. The longer the time for the insurance, the higher the cost. The closer the strike price is to the current price, the higher the price. Additionally, volatility influences price. The greater the volatility, the greater the cost. The simplest way to talk about pricing is to compare it to like pricing car insurance. A teenager driving a Porsche is much more expensive to insure than me, a 50 year old guy driving a minivan.

KK: What do you think are some barriers to entry to use price insurance? How can we get more cooperatives to participate?

AS: The first thing is teaching. People can’t use tools that they don’t know about. Like the introduction of tractors and fertilizers, it needs an introduction first. Maybe you don’t use the tool — it’s not the right tool for your job, but you need to know about it. The second is getting cooperative members to learn about this, not just the cooperative leadership.

KK: What role should the exporter play in this process?

AS: Well. Sometimes, yes, the exporters can facilitate the process. Sometimes the exporter… it’s not quite a conflict of interest, but they don’t want to be offering the cooperatives insurance services. What’s the conflict of interest? Well, someone has to put the money to purchase the insurance. Sometimes it’s the exporter. There is an additional concern for the exporter. You just “made” $100,000 on an insurance product, which you have just passed through to the cooperative. Now you have to report a taxable gain on your insurance windfall. And exporter has to pay taxes on a windfall wasn’t theirs.

KK: What do you want to tell the readers of Coffeelands about price insurance?

AS: [There are] lots of examples of people using these tools. It’s a real game changer for the users. One example: The price was $1.13 and one of our clients didn’t want to sell but had to deliver on a contract. He covered, the market turned to $2.00. [He] sold at $1.13, but the insurance returned 60 cents per pound to the producer.

In closing, PRM should be a tool for a cooperative, very much in line with the technical tools that we use on the farm. These tools are not inherently not speculative in nature. Rather, they are meant to remove speculation in your business. Properly applied, it will reduce the price volatility and improve cash flow to the farmers.

Kraig Kraft

Kraig Kraft is the CRS Technical Advisor for Coffee and Cacao for the Latin America/Caribbean. He is Based in Managua.

Comment

1 Comment

Comments are closed.

No mention of speculators in regards to the price of coffee being below production?